Why are we stuck with ACH? We have a Real-Time Payments (RTP) network (TN11)

Major banks are already on a real-time payment (RTP) network. Why does it feel like we're stuck with ACH?

🇺🇸 Happy Independence Day to U.S. subscribers! I hope you all enjoyed the long weekend!

📈 The newsletter grew by 5% in the past week. If you're new, welcome! Glad you're here.

📧 If you have friends, don't keep them hanging. Forward them this email or send them a link.

🗑️ I've received emails that my newsletter lands in spam/promotions for some of you. Kindly mark it as "Not Spam" or move it to your inbox if this happens to you. Let's dive in.

How do you send money to a friend? Most young Americans would answer Venmo or Cash App. Both services offer real-time payments, but Paypal and Square own them. Private services can provide real-time payments by settling transactions internally. Things get more interesting when you zoom out a bit.

How do you send money to a friend's bank? Zelle is the obvious choice if both your banks are on the network. It also offers real-time payment settlements. But what if one of you isn't banking with a Zelle-supported bank? What if you don't have Venmo or Cash App?

ACH becomes the generic answer. The ACH system in the U.S. was established in the 70s. Payments take two to four days to clear and are reversible. In today's world, the system rightfully feels archaic. The lack of instant liquidity can make or break small businesses. The system has improved since the 70s – your employers may already be paying you using the updated same-day ACH system. It's not real-time, but transactions are processed during the same day, provided they are submitted within one of the two windows.

I'm not talking about any of the above. I'm not talking about wires either because they are too expensive. The real-time payment system I'm referring to is the aptly named RTP or Real-Time Payment launched in 2017. U.S. banks released an RTP system almost half a century after Japan. I think this was a race it didn't need to win because real-time payments were less crucial in the 70s and 90s. The world wasn't as connected, and things moved much slower.

But it is finally here, and it settles payments in two to three seconds on average. Instead of ACH's batch processing, RTP settles payments individually. Twenty-four hours a day and seven days a week. No more days off on weekends or holidays.

The system works by settling funds in the background using an account that both banking parties must keep above certain thresholds. Unlike ACH, the system requires your bank to confirm that you have the funds before approving the request to withdraw it.

The system sounds fantastic, but it feels invisible. According to The Clearing House, many banks are already integrated with the system. While banks already offer RTP to corporate clients, consumers are still stuck with ACH and maybe Zelle. If I wanted to send money between my accounts at different institutions, I have to use ACH unless they both use Zelle. Even with Zelle, the service is not intelligent enough to send my money to my account at a different bank on the same network. I have to hack around their limitation by using my phone number for one account and my email address for the other. It doesn't feel like we have real-time payments in the U.S. because banks haven't enabled it for peer-to-peer payments.

Popular apps people deposit money to don't support RTP either. Robinhood and Coinbase don't let you use 100% of deposited funds till it has cleared after two to four days. Many fintech solutions still don't offer real-time payments today.

Dwolla, the payments API platform, announced its integration with the RTP network three months ago. Dwolla is the top ACH integration platform choice for many fintech companies. Thanks to modern infrastructure and the composability of APIs, Dwolla should be able to offer its customers real-time payments with minimal changes to their existing integration.

Real-time payments aren't common now, but I bet they'll be the status quo in a few years. It's only a matter of time.

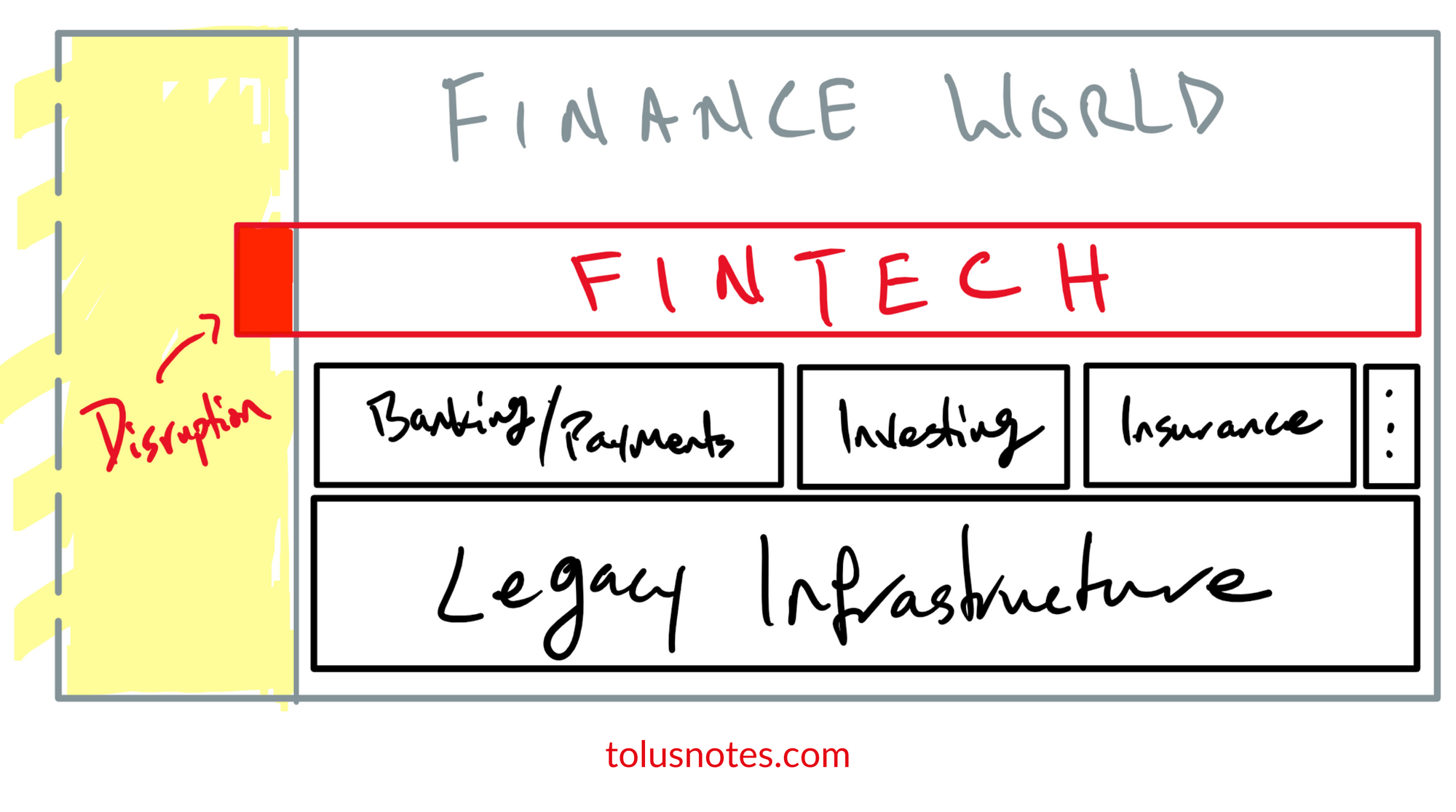

FinTech x DeFi

I recently emerged from the crypto rabbit hole when it hit me: Fintech failed at disrupting the finance space. However, when I dug deeper, I found out that it was due to primitives. Fintech companies had to make due on legacy infrastructure. Now that they are maturing, they'll start to roll out their own infrastructure and offer new services. The interesting part of this is that the features they'll start rolling out are already getting adopted in DeFi.

Read part 1 of the new series I'm working on. It's exploring the intersection between fintech and DeFi, and what we can expect from both in the future. Here's a quote:

Fintech has done a lot so far, but founders limited their scope of innovation to what can be built on the legacy infrastructure. They continue to rely on those they should be disrupting.

Part 2 will dive even deeper. I'm currently at 4000 words and should have it ready late this week or next week.

Weekly Chart

This mysterious chart will be revealed in the next post later this week or next. Email me your guesses.

What to Read

Tolu Salako

Tolu Salako

I recommend reading the FinTech post. My follow-up pieces will require it for context.

Tolu SalakoI also have a dedicated "What To Read" page where I dump all of the most insightful pieces I read that week. Check it out.

Sources

https://www.moderntreasury.com/journal/real-time-payments-around-the-world#3

https://www.theclearinghouse.org/payment-systems/rtp/rtp-participating-financial-institutions

https://www.theclearinghouse.org/payment-systems/rtp/institution#show-hide-content-2fb9c156-287a-4921-8196-65d9175b8b3d

https://www.theclearinghouse.org/-/media/new/tch/documents/payment-systems/rtp_-pricing_02-07-2019.pdf

https://www.prnewswire.com/news-releases/dwolla-unlocks-real-time-payments-301262368.html