The True Cost of FDIC & Stability — Brokerage Accounts are the new Savings Accounts (TN12)

People saving and relying on the FDIC may be exposing their capital to other risks. Fintech apps blur the lines between risk-off savings and risk-on investment accounts.

🍉 Happy National Watermelon Day!

📈 The newsletter's growth was flat the past week.

📧 If you have friends, don't keep them hanging. Forward them this email or send them a link.

🗑️ I've received emails that the newsletter lands in spam/promotions for some of you. Kindly mark it as "Not Spam" or move it to your inbox if this happens to you. Let's dive in.

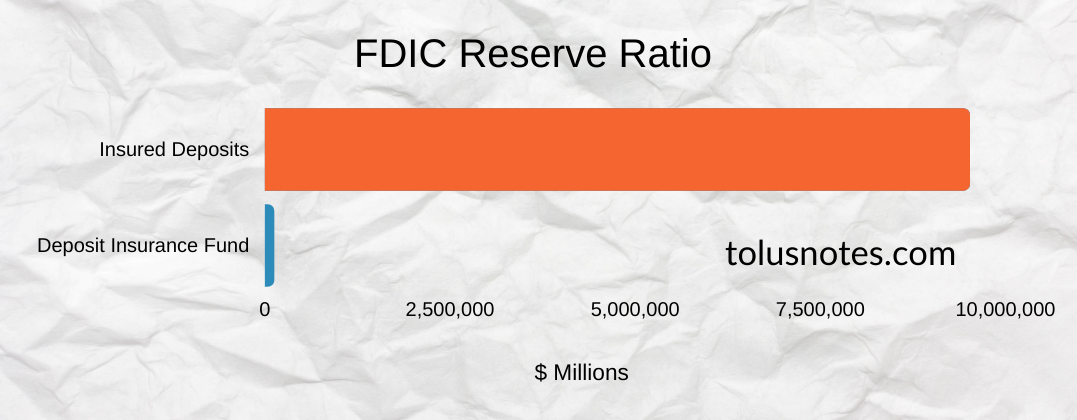

Most people are familiar with the FDIC. They protect depositors when a participating bank fails. The advent of FDIC has largely prevented large-scale runs on banking institutions. During the stock market crash of March 2020, most people didn't rush to withdraw their money from banks because they weren't scared of losing their money. Since its inception in 1933, FDIC-insured depositors haven't lost a single penny. But there is a catch. Like any other insurance, it works as long as claims are sporadic. The FDIC can't repay everyone if all banks were to fail simultaneously. The FDIC reported that their deposit insurance fund is about $119 billion as of March 2021. In the same report, the deposits the fund covers totaled about $9.5 trillion. For every insured dollar, the FDIC has about 1.25 cents [1].

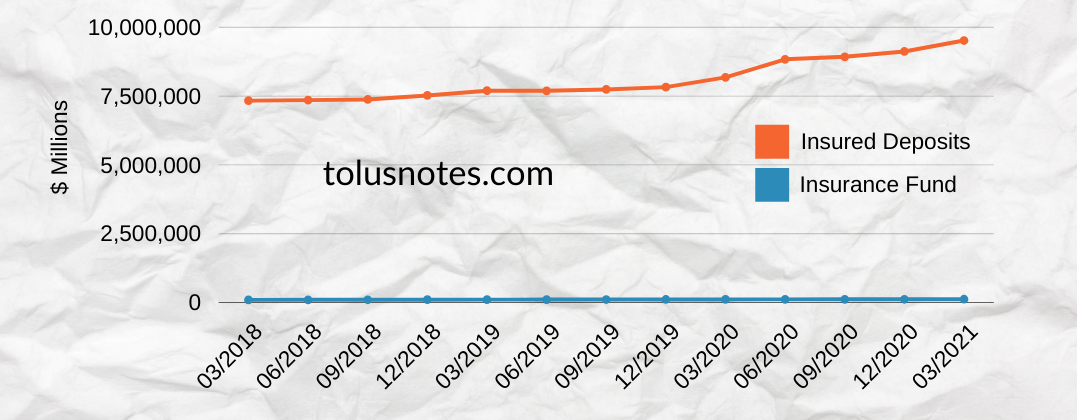

Here's how the insurance fund has grown relative to insured deposits.

If every bank were to fail instantaneously, we'd have bigger problems than FDIC. But assuming it happens, the FDIC has a line of credit with the U.S. treasury. The U.S. government guarantees the remaining deposits after the FDIC exhausts its options. This can happen indefinitely because the treasury can always issue more debt. It then becomes a question of how you feel about U.S. debt compared to GDP, but we won't get into that today. Large-scale bank failures are unlikely because banks are supervised and regulated by the Fed, OCC, and the FDIC. We can assume that the U.S. Treasury (via the FDIC) can cover deposits in most cases.

In the past, people could save their way to retirement without investing. That option is no longer available to the younger population. The FDIC protects deposits when banks fail but is powerless against inflation. The problem is that banks no longer fail as often as they used to, but the fear of inflation (which is just as serious as inflation itself) is more rampant than it used to. We live in a negative real yield environment today. Anyone "saving" outside of risky or inflation-protected assets is losing money. Risk-off money in savings accounts, even high-yield ones, are no longer preserving capital.

The New Savings Account

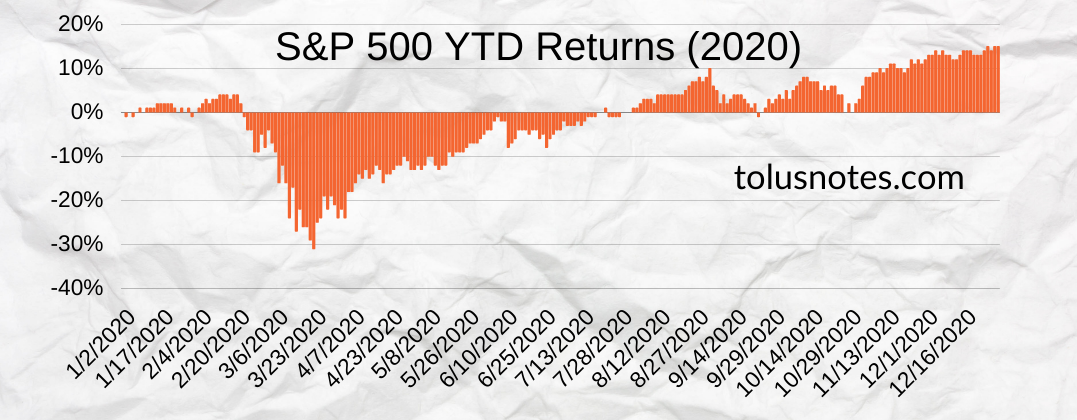

We experienced one of those near-impossible scenarios in 2020. Every business or activity that wasn't essential or online was forced to shut down. The stock market plummeted and rebounded almost instantly. Historical records will show that the S&P 500 returned 16% in 2020. Unless you dig in, you won't know that it crashed over 30% in thirty days. I wrote about the experience here, here, and here. Zoomed out, 2020 was a banner year largely thanks to swift actions by the central bank and the U.S. government.

But there's a side effect to what happened that year. The Fed set a precedent, and as Ben Carlson wrote about the topic, "you can’t stuff that genie back in the bottle once it’s out." Investors will expect (and likely demand) this level of involvement the next time we think we're experiencing something similar to 2020. The event may be worse, or it may not even be remotely close, but voters will demand stimulus checks, and investors will expect the Fed to step in. It means that the "money printer" is here to stay. I recently wrote about how this expectation has enabled funds to take on more risk. Cathie Wood's ARK Invest, for example, is leveraging it.

In this new world, the Fed insures the market by guaranteeing liquidity just as the government guarantees FDIC-protected deposits in savings accounts. This is an odd take and I'm almost laughing typing these words, but there's some truth to it. Investors expect higher returns for participating in the market. The typical long-term investor makes money largely by not selling during market crashes. It usually comes down to perseverance. In this new world, the Fed shortens that waiting period during market downturns.

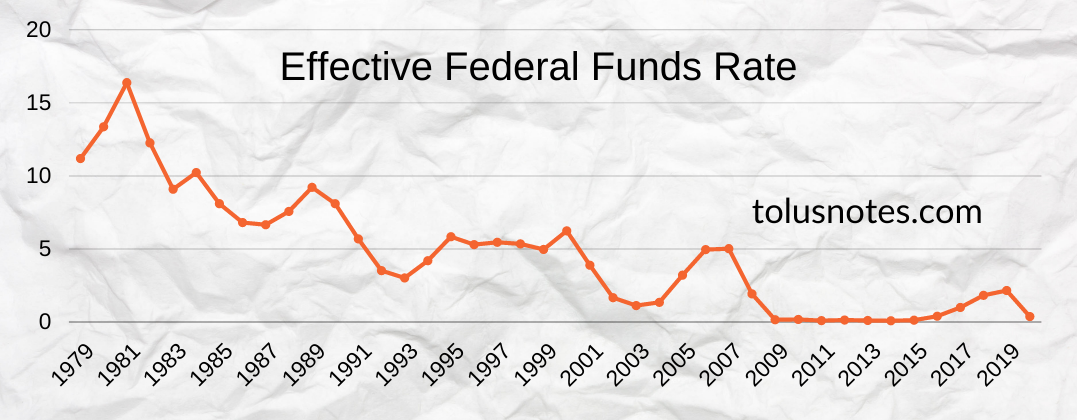

But there's a catch. There always is. The more rates are cut, the less effective it gets. At our current levels near zero, the Fed can't cut rates to respond to a recession without going negative. We had this insurance, but we've used it all up. The Fed is expected to raise interest rates sometime next year. But every significant rate cut since the 1980s has resulted in lower highs. The U.S. could indeed be heading towards uncharted territory. We've never been in a negative interest rates environment like they have in parts of Europe where people pay to save and are paid to borrow. Banks can absorb the costs of negative interest rates for a while, but depositors eventually have to pay to keep their money safe.

Risk-Off <> Risk-On: Fintech Gets It

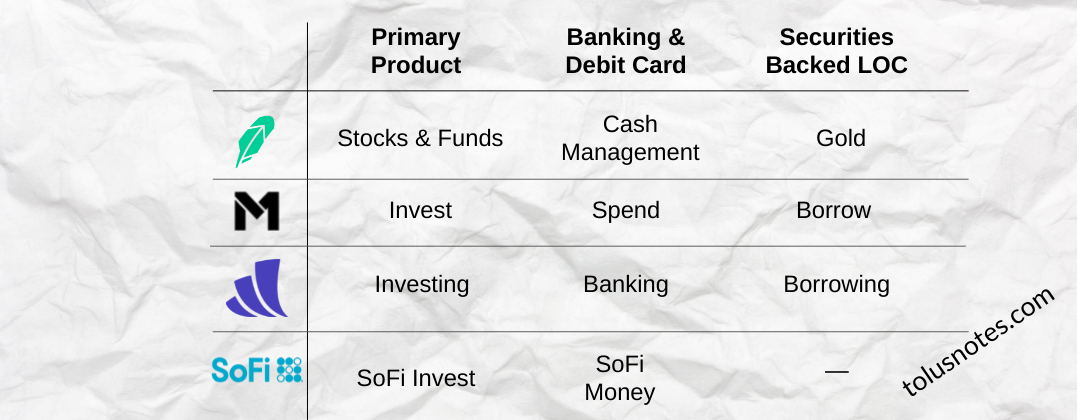

Non-productive risk-off behavior is discouraged where we're headed. The savings account is dead, and fintech knows it. The most successful fintech services blur the lines between risk-on and risk-off money. Today, popular investing apps also offer fully functional banking accounts with a rewards debit card. While this isn't novel, modern brokerages like Robinhood and M1 Finance erase the lines between investing and banking. By allowing seamless and instant transfers between investment and bank accounts, you essentially end up with a single account. A brokerage account that allows you to spend your cash reserves and earn rewards on your balance and spending. It's safe to assume that consumer fintech apps want to be the one-stop shop for all things money. Chime will eventually get into investing, and Cash App will enable lending. I think those that already offer risk-on services have a leg up in this race, but that's a topic for another time.

Further Reading

The Long Decline of Global Interest Rates

Weekly Chart

From CNBC:

Federal criminal fraud charges against Trevor Milton accuse the Nikola founder of lying about “nearly all aspects of the business.”

He was released on $100 million bail secured against two of his properties in Utah. Here's the zoomed-out version of the stock.

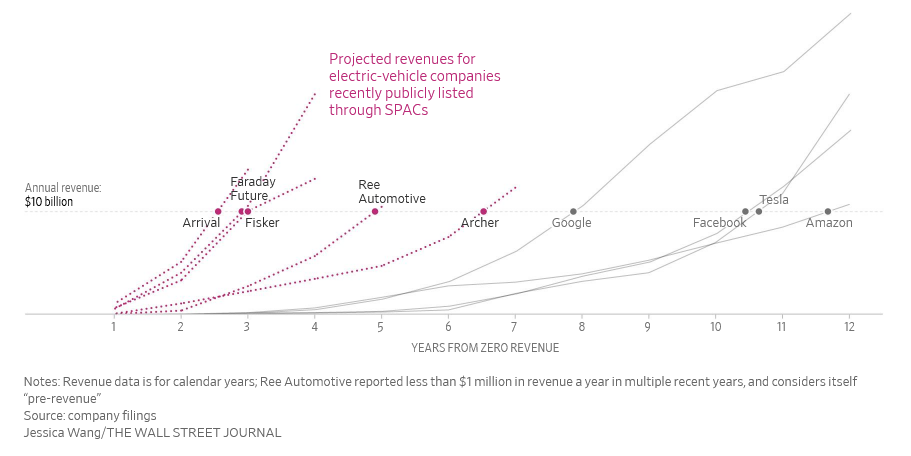

A very nice reminder that investors should ignore SPAC revenue projections.

What to Read

On ignoring revenue promises:

Tolu Salako

Tolu Salako

If you've been hearing about DeFi and smart contracts and want a quick rundown from the perspective of a stock market investor, here you go:

Tolu Salako

I added an /about section to the blog after one and a half years of publishing. Check it out.