Taking Ls like a Hedge Fund

You should be skeptical when someone promises out performance for a fee

A subscriber requested my take on Titanvest - a robo advisor that attempts to beat the market by following hedge funds and creating a personalized hedge during downturns. First of all, I appreciate and welcome the engagement. I'm always delighted to hear from you all. Second, I wouldn't touch Titanvest or any other hedge fund promising out performance for a fee. Here are my reasons.

Data says otherwise

Picking individual stocks hasn't worked well for active managers in the past, but they spice it up by following the most common holdings of elite hedge fund managers. Without a full understanding of how they select hedge funds, we won't be able to determine how they end up with 20-30 all-star stocks, but we can assume that hedge fund managers are active, meaning that they pick stocks, and that Titanvest is also active by picking stocks from a poll of hedge funds that they've filtered using their elite criteria. We can think of it like a funnel: Hedge funds -> Titanvest's elite hedge funds -> Elite hedge fund stocks -> Titanvest stocks.

These managers tend to be great at identifying high-quality companies.

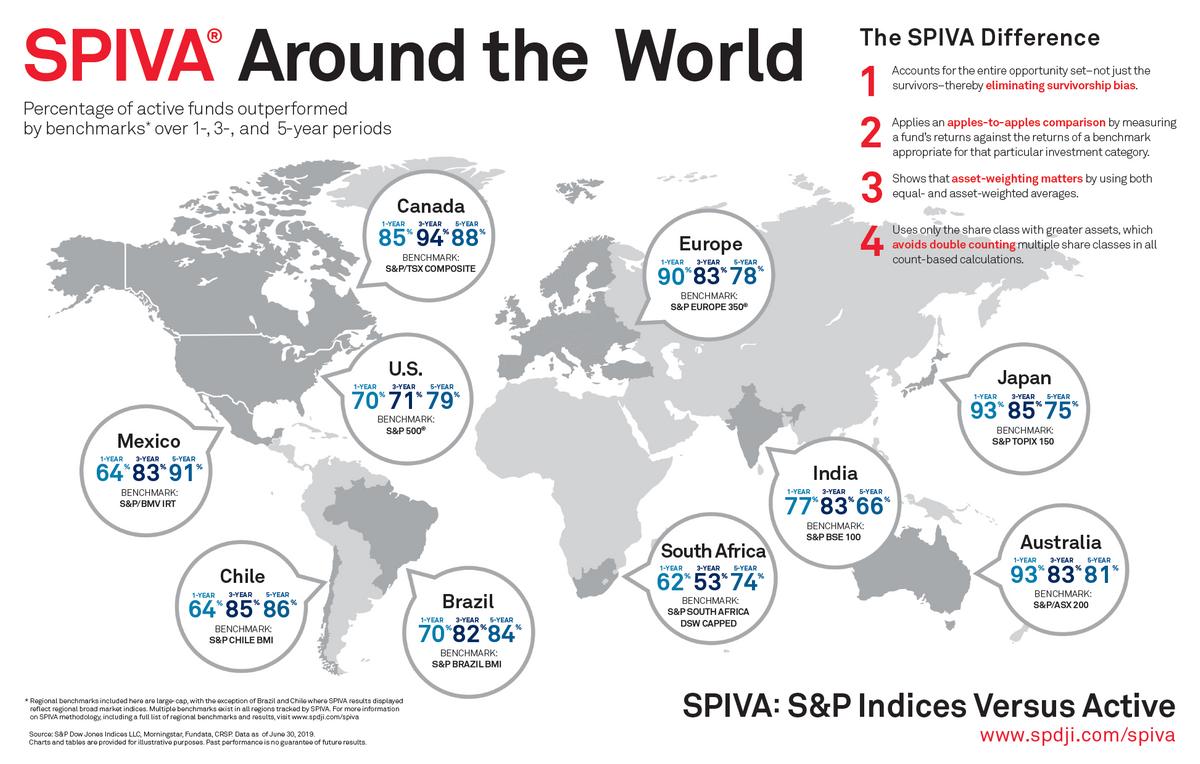

Globally, active funds have under-performed benchmark indices. South Africa's active managers seem to be doing the best job, but let's focus on the U.S. active managers who, according to the data from SPIVA, have under-performed for the ninth consecutive year. All this during a bull market where almost everything goes up, literally. It is almost impossible to continue to successfully identify managers who then continue to successfully identify stocks that go on to outperform.

While some, like William Sharpe, believe that it is impossible for actively managed funds to outperform passive investing after costs, Titanvest thinks that they can do better. They're so confident that they only limit their pool of securities to whatever the elite hedge funds are buying and selling.

Buy high, sell low

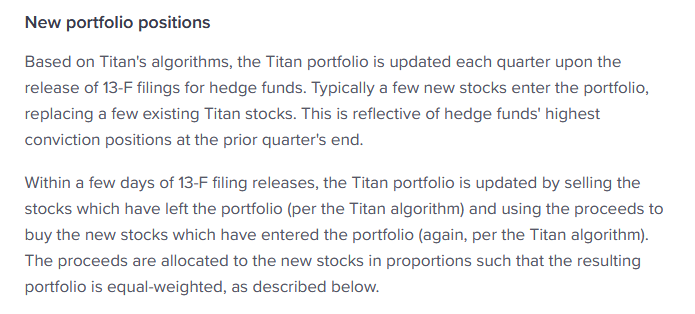

13-F filings provide insight into what hedge fund managers are holding. The only problem, for Titanvest, is that those filings are due within 45 days after the end of the calendar quarter. So when a fund they follow decides to drop a stock, they usually won't be notified till the 13-Fs are public. Theoretically, the hedge funds could start reducing positions at the beginning of the quarter, and Titanvest would be actively buying from them. By the time Titanvest decides to drop the stock, it may have been beaten down due to the downward momentum caused by other investors dumping it for the same reason (they aren't the only ones following 13-Fs). This is especially bad for newer members who join their platform. Those members will get hit the hardest because their portfolios are equally weighted, and they'll see a sharp decline in this scenario. Now, if you flip the script and make it an upward momentum, Titanvest still won't benefit because they only open positions after 13-F filings are made public. Infact, they could be overpaying due to other 13-F followers buying at the same time.

Putting the hedge in hedge fund

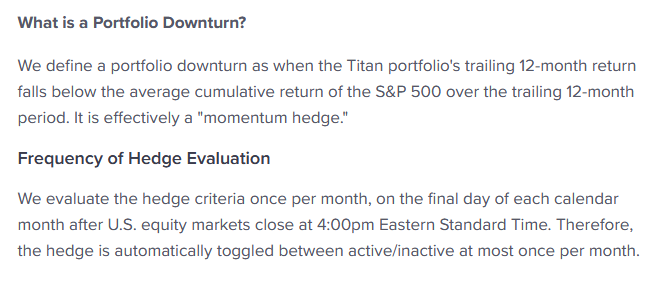

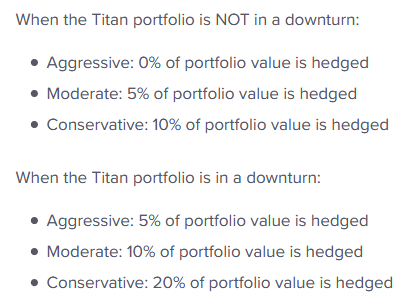

One of the things that may be worth paying for is their personalized hedge which most retail investors are not comfortable doing themselves. Yet again, they've fallen short in this regard. Short positions are activated when Titanvest under performs the market, not during a market downturn. You read that right. If their trailing 12-month returns are lower than that of the S&P 500 during the same period, they hedge a percentage of your portfolio. Data shows us that active managers like Titanvest will underperform over time, but Titanvest is deciding to inverse the S&P 500 whenever they're losing. They could be inversing the market simply because of some horrible stock picks. Not only would investors be missing out due to sheer under performance, they would also be losing money by selling securities to activate miscalculated hedges.

One more thing - the advertised personalized hedge isn't personal at all. The percentage of the portfolio that's shorted is personal in the sense that investors are given 3 options based on their risk tolerance. But for the fees they charge, they're not really creating a personalized hedge. A truly personalized hedge would consider all your holdings within and outside the fund along with the industry you work in and so on. Instead, they inverse the market index even though they're only holding 20 to 30 stocks that don't necessarily represent the market.

Could it work?

There is a chance that they've figured out the holy grail of increasing alpha. In Systematic 13F Hedge Fund Alpha by Mobeen Iqbal, Farouk Jivraj, and Luca Angelini; they found that value exists in 13-F filings. After accounting for the 45-day lag, they found that the strategy delivered a statistically significant six-factor alpha relative to the S&P 500. But they also mention that "the ‘who’ and the ‘how’ must be considered in equal weight when attempting to systematically extract alpha from 13F filings." I give Titanvest some credit for trying, but I'm not convinced they've figured out how to pick hedge funds. They may do well in the short term, but past performance, even for hedge fund managers, does not guarantee future performance. Tiger Management and Long-Term Capital Management are great examples of hedge funds that did exceptionally well before losing everything.

Conclusion

Investors looking to outperform may be drawn to funds like these due to its exclusive nature. Being part of a fund that's not readily available to others may make it seem like a good idea to invest, but keep in mind that the whole point of investing is to have your money make more money. The odds of making more with funds like Titanvest are not in your favor. It is true that a more concentrated portfolio could potentially have more significant returns, but it isn't guaranteed. We diversify because it is almost impossible to predict which company will have the highest returns. Even if we're right about the potential of a company, we have no control over how the stock performs.

I've written about how young investors can improve returns by investing the time they have left in the market. Those who can stomach even more volatility than what's described in that post may want to consider leveraging. It sounds scary on the surface, but the math checks out for most young adults.

When trillions of dollars are managed by Wall Streeters charging high fees, it will usually be the managers who reap out sized profits, not the clients. Both large and small investors should stick with low-cost index funds.

- Warren Buffet

💬 Provide feedback by replying or emailing me at newsletter-at-tolusnotes.com

❤️ 30 people are now subscribed to these notes. Give the gift of Tolu's Notes for valentine's day weekend

🏆 Oscar-Winning Parasite may be worth your time. I enjoyed it

📚 Still Reading Fewer, Richer, Greener

Tolusnotes participates in Amazon Services LLC Associates Program. We earn a small revenue from qualifying purchases.