Robinhood Competes With TikTok and Instagram, Not TD Ameritrade or Charles Schwab

The last thing your money needs is more user engagement. Investors are better off using

👊🏾 Welcome to Tolu’s Notes — I cover risk taking and decision-making. If you are new, join my weekly mailing list here

Robinhood is responsible for getting millions of retail investors into the market. They deserve credit for making investing more accessible to the average individual. Their offering is primarily free, uncluttered, and most importantly, it's intuitive. I bought my first stock around 2014 using TD Ameritrade. Unlike what Robinhood offers, I had to pay commissions, the site was ugly (it still is), and it almost seemed like I shouldn't be investing because of how complicated the system was. Today, TD Ameritrade, along with other major brokerages, no longer charges commissions for trading shares, but their platforms still aren't user-friendly. I'm used to it now, but I can't imagine getting started today without a modern user interface. Kudos to Robinhood for helping the average individual believe that investing is also for them. As a society, we needed this shift. More people are willing to put their capital to work thanks to Robinhood. They have changed what it means to be an investor. With that said, serious investors should avoid Robinhood because the same features that make it fun for the new guy to start investing make it extremely difficult for virtually anyone, regardless of experience, to stay invested.

Gamifying Money

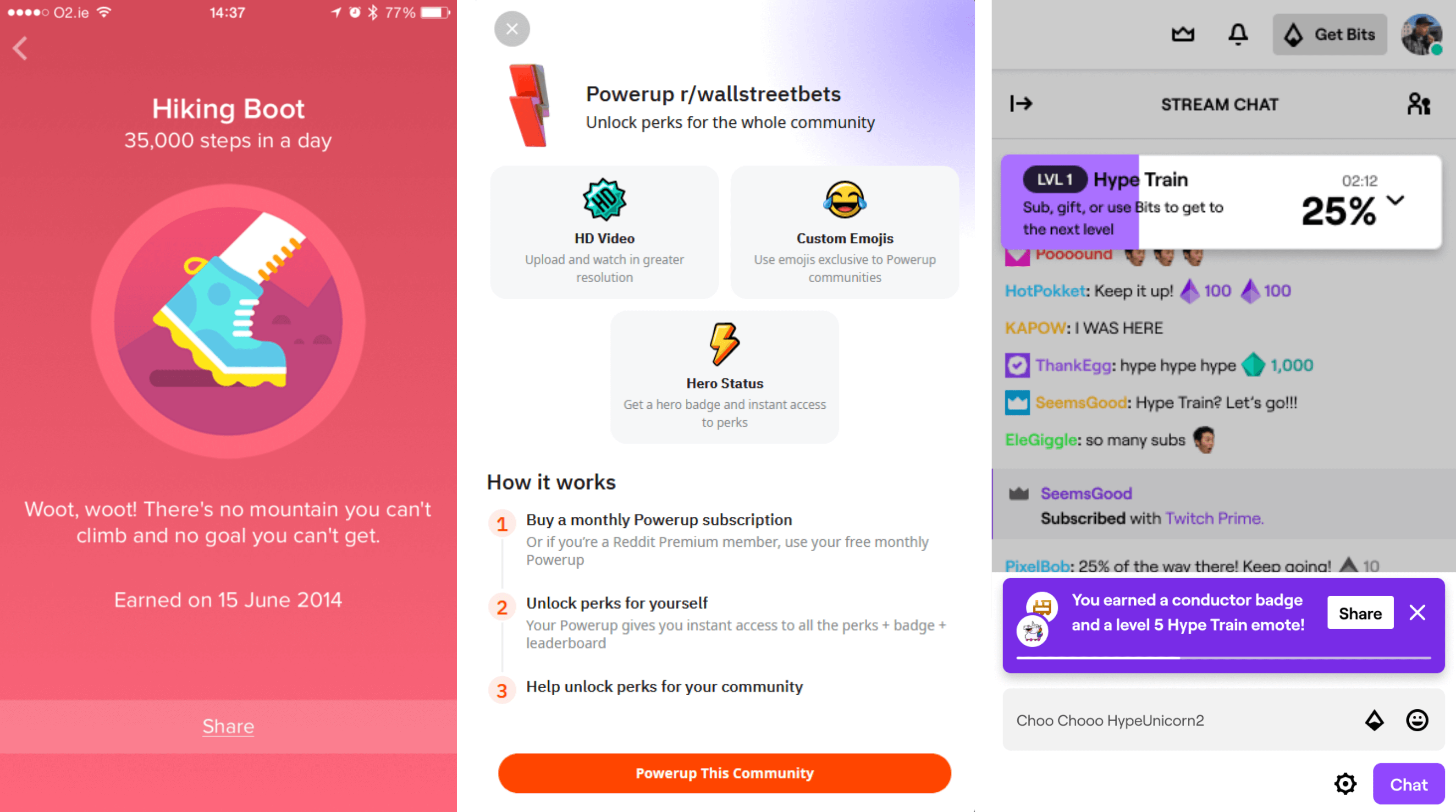

Gamification happens when gameplay elements are present in unrelated contexts. Think of powerups on Reddit or badges on Fitbit. Some services are so gamified that they have become games. Many streamers and viewers may not realize it, but Twitch is a game [1]. One with tiers, points, challenges, rewards, collecting, exchanging, and leaderboards. Hype Train, anyone? Companies go through all the trouble to gamify their platforms because it drives engagement. If you still doubt the power of a gamified experience, look no further than Starbucks Rewards. Their loyalty program alone holds a more significant cash balance than some banks [2]. Having your customers come back on their own is more profitable than advertising to bring them back. It works amazingly well for companies. Unfortunately, the habits formed through gamified experiences aren't always in the interest of their customers.

Similar to the apps discussed, Robinhood aims to get its users hooked on its products. The overly simplified app, confetti, animated account balance, and colors that pop all gave first-time investors the boost of confidence they need to make their first trade. Afterward, Robinhood sends a never-ending barrage of notifications designed to keep investors within the app. The effect of these notifications compounds with the persistent noise that is the stock market. These things are great for Robinhood's user engagement scores. But the last thing your money needs is more user engagement. The less you act, the better, but Robinhood continues to invite you to take a peek and continuously nudges you to make decisions. [3]

Robinhood’s mission is to democratize finance for all. We believe that everyone should have access to the financial markets, so we’ve built Robinhood from the ground up to make investing friendly, approachable, and understandable for newcomers and experts alike.

To Democratize Finance For All

I've spent the past few years studying decision-making and the relationship our brains have with money. One thing I've learned is that our brains prioritize survival above risk-taking. You've probably heard it a million times by now, but our ancestors didn't have time to contemplate if a bush was moved by the wind or by a hungry lion. They quickly learned that those who got curious got eaten most of the time. In investing, this survival behavior is destructive. Investors that panic whenever the wind blows are often the ones that get eaten. Those that are curious, or the contrarians, fair better. It may seem obvious if you've been investing for a while, but you only have to chat with a few new investors to realize what our default behavior is when it comes to losses and gains. For most people, buying comes easier when prices hit new records than when they hit new lows.

That is where Robinhood falls short of its mission to democratize finance for all. They make it easy for the retail crowd to start investing, but they aren't interested in keeping them invested. To democratize finance is not only about making it accessible but also about making it easy to understand. There's no point in a fantastic tool like Robinhood if most people can't use it well. One can make the argument that it isn't Robinhood's job to educate, and if it were any other brokerage, I'd agree with you. But their mission is to make investing approachable as well as understandable. They don't need to babysit investors at all. Instead, they need to do a little less nudging after an investor makes that first trade.

I understand that trading is how Robinhood makes most of its money [4]. Incentivizing their users to hold instead of getting in and out of positions is probably never going to happen. Robinhood cannot survive on Gold alone; payment for order flow is their bread and butter. For these reasons, I can only recommend Robinhood for Meme Portfolios. Serious investors that are interested in the long-term success of their portfolios should look elsewhere.

The App That Cared

This section is an aside, but one of the coolest popups I've ever received was from Personal Capital. I think I opened the app during some odd hours, maybe around 1 or 2 am, and got a warning about the health effects of checking on my finances that late at night. I only received it once, and they probably turned off that A/B test years ago, but I will never forget it. I felt like an app that shouldn't even bother cared about my mental health.

There's Power in Design

Another aside, but the first time I tried Robinhood was in 2017. The investing experience it offered felt like magic compared to the world I was used to. My ACH transfers seemed to be faster, I could immediately redeploy proceeds from stock sales, and it felt great to watch my account grow. Looking back on my old statements, I had Robinhood Gold — their premium membership plan. They were able to convert me into a paying user after a month of using the app. Regular accounts still needed to wait for the 3-5 day ACH delay and the t+2 clearing house settlement delay. Like everything else Robinhood offered, Gold was friendly. Signing up was simpler than their competitors, and Robinhood granted access immediately. Sticking with Gold was even easier. At the end of every month, I knew exactly how much I owed. The flat rate could have cost me more in interest, but it didn't matter. The terms were clear and concise. Product-wise, Robinhood won me over, if only for a bit.

Sources

[1] Twitch is a game - https://www.rewardco.com.au/twitch-is-the-ultimate-example-of-gamification/

[2] Starbucks has more money than many banks - https://www.marketwatch.com/story/starbucks-has-more-customer-money-on-cards-than-many-banks-have-in-deposits-2016-06-09?mod=mw_share_twitter

[3] Robinhood Design - https://www.nbcnews.com/tech/tech-news/confetti-push-notifications-stock-app-robinhood-nudges-investors-toward-risk-n1053071

[4] PFOF - https://www.cnbc.com/2020/08/13/how-robinhood-makes-money-on-customer-trades-despite-making-it-free.html