Personal Human Capital & Labor Income — are you a stock or a bond?

Given your job and future income expectations, would you consider yourself a stock or a bond?

It's an age-old question in investing. Countless researchers have sought to figure out how to optimize portfolios by taking an investor's human capital into account. Initial versions of this asset allocation problem focused on the investor's retirement status and how much longer they expected to be employed. Their research gave birth to rules like the 100 minus age rule. For many years, investors used this rule to determine how much they should allocate to risky assets like stocks vs. safer or bond-like assets. For example, a recent college graduate joining the labor force for the first time at age 22 will hold a portfolio consisting of 78% stocks and 22% bonds. As they got older, the rule dictates they move some money out of stocks into safer assets like bonds. Target-date index funds like Fidelity's FDEEX try to do something similar. However, some like Ian Ayres & Barry Nalebuff [1] suggest anywhere from 100% - 200% equities in a leveraged portfolio at a young age. This question is known as lifecycle investing (though purists don't entertain the use of leverage). Instead of allocating capital solely based on their current net worth, investors are advised to take the present value of their future labor cash flows into account.

To W2 Or Not

The historic lifecycle approach has typically treated that future income as a bond or fixed-income. Young individuals seem more employable, and they don't have much of a portfolio. A recent grad will typically have less money in the market than a veteran in the same field. This thinking categorizes young individuals (their future cash flows, not the human) as bonds, thus encouraging them to hold substantially more equities to balance things out. As a young investor, it's easy to fall for this assumption if you've never experienced any uncertainty with your income source.

W2 employees (young or seasoned) expect a check from their employers regularly. They don't have to worry about tomorrow because they worked for someone else today. This relationship behaves like fixed-income security that pays out interest regularly without many surprises. If they made $5000 last month, they expect to make $5000 this month (assuming they didn't get a promotion or a pay cut). In addition to this, younger employees are expected to receive multiple raises throughout their working lives. With that in mind, their non-tradable fixed-income seem even more massive.

Entrepreneurs are different. There is less certainty around their income. A small market change may not affect W2 employees, but it could wipe out entrepreneurs. Take, for example, Google's SEO changes. Each time Google updates its ranking algorithm, it shifts billions of attention from site to site. One of the updates they released in 2015 favored mobile-friendly sites. Entrepreneurs who never had to worry about mobile optimization had to start paying attention. Websites that were mobile-friendly when it didn't matter got rewarded if their competitors got complacent. For reasons like these, entrepreneurs seem more stock-like. They are more vulnerable to market forces, but those same forces could significantly work in their favor.

Co-integration Effect

Simple lifecycle rules bake in the assumption that young investors have a secure source of income. Unlike retirees, they are flexible enough to find another job if they ever got fired during a recession. They're advised to hold more stocks since their income is separated from the stock market. Some researchers question this notion that underpins many lifecycle claims. Benzoni, Collin-Dufresne, and Goldstein (2005) found that the stock and labor markets are cointegrated in the long run [2]. Pay attention to the word: co-integration. It is different from its common substitute: correlation. With cointegration, variables (series) don't have to move in the same direction, but the distance between them will mean-revert over time. This means that a young investor's future labor income is highly exposed to market returns and market risk. They concluded that due to this co-integration effect, the optimal move for working young investors is to take a substantial short position in equities. Middle-aged investors, however, are less exposed — meaning, their future labor income is more bond-like. They advise this group to take a larger position in risky assets. Finally, at retirement, the expected value of future income is zero. Retirees aren't stock-like or bond-like, so they are advised to reduce their exposure to risky assets.

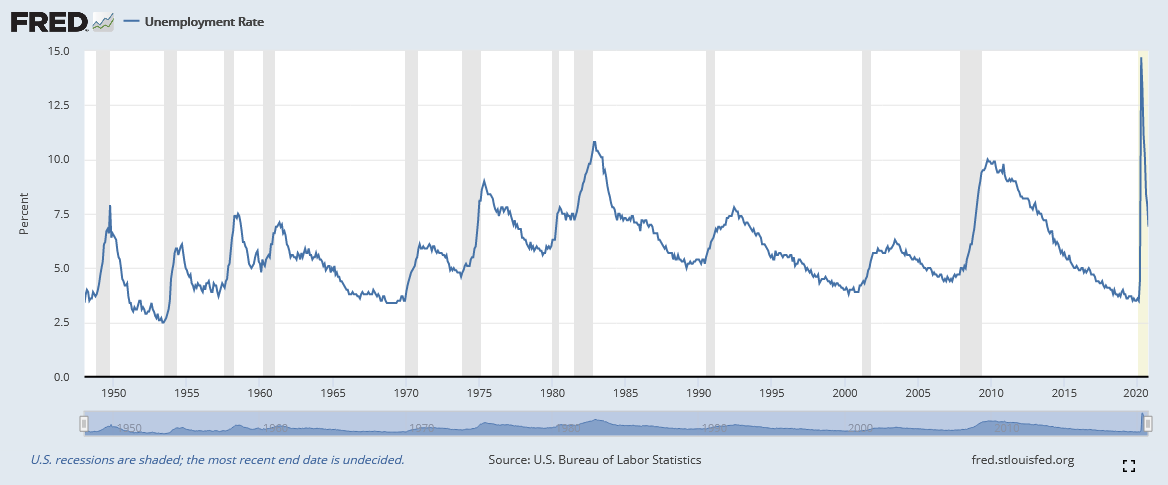

Empirically, I agree with the co-integration claim. Economic recessions that affect stock prices also cause a spike in unemployment. When the stock market is doing well, companies typically hire more and give out more raises and bonuses. When we expect less from the stock market, companies become more cautious and focus on preserving cash for the rough road ahead.

Take 2020, for example, where the government closed down most businesses to combat the coronavirus pandemic. The shock affected both stock returns and labor income. For risk-averse investors who assumed that their income was bond-like, mid-March 2020 was an important test. Many young-working investors lost their jobs (guaranteed future labor income) or businesses as well as a good percent of their retirement accounts. When lockdowns began, small business owners suddenly had $0 in revenue for themselves or their employees. Big corporations saw their share prices tank as they laid off millions of employees that they could no longer afford to pay. All of a sudden, both W2 employees and entrepreneurs became stock-like. They may have been a bond every day leading up to 2020, but it meant nothing if that bond evaporated along with the stock market in mid-March 2020 when they needed the safety the most. The argument that young investors could easily find a new job doesn't hold if they were forced to sell when prices were low. Situations like these are what cash reserves are for, but investors who bit on too much risk learned a difficult lesson.

The good news is that the result of their research is susceptible to investor risk profiles. If the young investor is willing to take more risk than the investor modeled in the study, the optimal move would be to allocate a lot more capital to stocks despite the co-integration effect. This is supported by Ayres's and Nalebuff's paper (2008) [1]. They found that if (a big if) an investor could weather the storm and take a bit more risk, the optimal move would be to use leverage to gain exposure to more equities. I've written more about this paper and their book (Lifecycle Investing) below.

My Thoughts

Lifecycle approaches aren't silver bullets. Researchers have found that merely holding the S&P 500 is far superior to many of these rules [3]. I also worry about people getting fooled by randomness. Most of these researchers base their models on historical returns (not saying there's an alternative). History has favored equities in the U.S.; therefore, equities seem to come out ahead mostly. Finally, remember that the entire point of investing for retirement is to avoid dying broke. You lose the game if you end up with nothing at retirement. What you had before crossing the finish line is not important. You eat your dollars, not your return.

Human Capital — A Portfolio

This section is an aside, but I like to think of human capital as a portfolio. Labor income is only a portion that doesn't provide the full picture. There's a set of skills you possess that your employer (or customer) is interested in; that's why they choose to pay you instead of someone else. In addition to those, you have other intangible skills that may not immediately apply to your primary source of income. For example, you may be the best salesperson at your company who also happens to be a skilled gamer that people love to stream on Twitch. That skill is intangible, but the income potential is real. People also pay for creativity (music/art), information (education/leverage), and social skills (connections/emotional).

Unless you have controlling stakes, you can't decide how companies use your capital. However, the investments you make in your human capital can improve your leverage and provide more options.

Books

Lifecycle Investing – Ian Ayres and Barry Nalebuff

Fooled by Ramdomness – Nassim Taleb

Sources

[1] Ayres, Ian and Nalebuff, Barry, Life-Cycle Investing and Leverage: Buying Stock on Margin Can Reduce Retirement Risk (June 2008). NBER Working Paper No. w14094, Available at SSRN: https://ssrn.com/abstract=1149340

[2] Benzoni, Luca and Collin-Dufresne, Pierre and Goldstein, Robert S., Portfolio Choice Over the Life-Cycle in the Presence of 'Trickle Down' Labor Income (12/31/04). Available at SSRN: https://ssrn.com/abstract=651061 or http://dx.doi.org/10.2139/ssrn.651061

[3] Shiller, Robert J., The Life-Cycle Personal Accounts Proposal for Social Security: An Evaluation (April 2005). Available at SSRN: https://ssrn.com/abstract=703221

All content provided on this blog is for educational purposes only and should not be taken as personalized investment advice, not as an indication to buy or sell certain securities. The owner of this blog makes no representations as to the accuracy or completeness of any information on this site or found by following any link on this site. The owner will not be liable for any errors or omissions in this information nor for the availability of this information. The owner will not be liable for any losses, injuries, or damages from the display or use of this information.Tolusnotes participates in Amazon Services LLC Associates Program. We earn a small revenue from qualifying purchases.