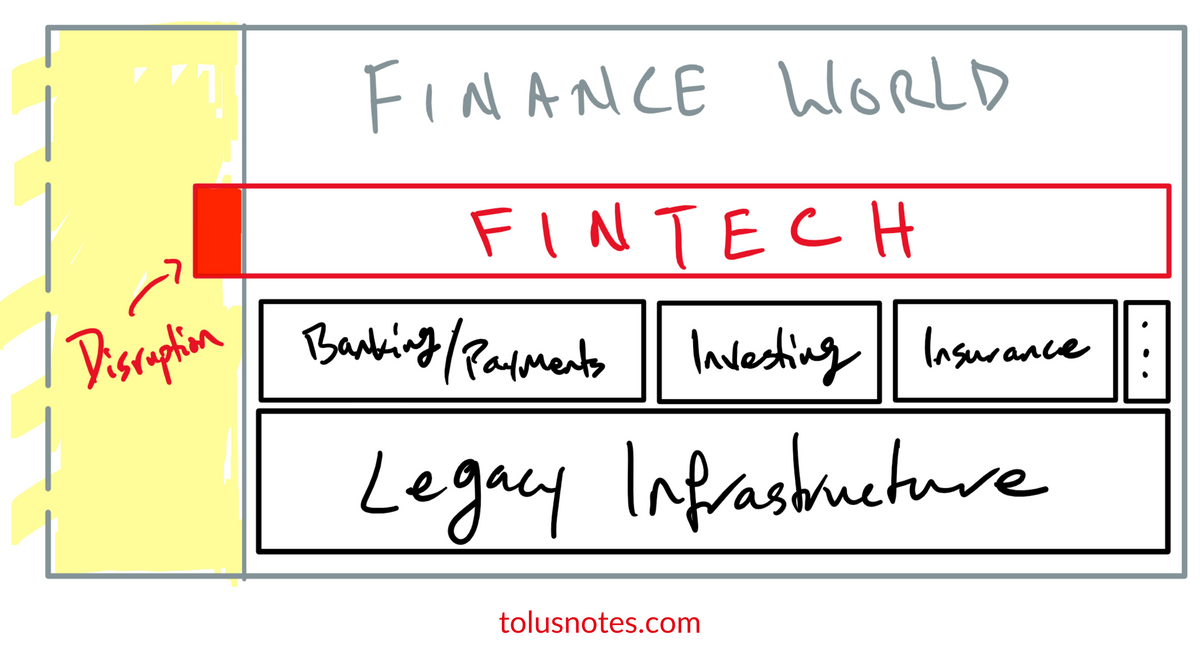

FinTech Didn't Disrupt Much (FinTech x DeFi – Part 1)

The legacy financial infrastructure in the U.S. has held back fintech innovation

When looking into technological revolutions, pay attention to how it changes the finance world. Known for being ancient and slow, the finance industry is quite disruptive. First, it provides the capital entrepreneurs need to build things that seem unreal and out of reach. Then it adopts new technology very quickly if it has the potential to make money. It's always looking to reinvent itself.

Whether it was gold ingots or information that they had to relay, banks were among the early clients of the penny post, the railways and the telegraph on the national level in the early days of the second surge, as well as of international railways, telegraph and steamships, together with telephone, typewriter and calculator from the beginning of the third revolution.

— Carlota Perez, Technological Revolutions and Financial Capital, p. 96

From railways to the telegraph, the finance world is early to adopt technologies that can increase the speed and fluidity of money. Banking is a great example. Not that long ago, you had to walk into a physical bank to use their services. Today, however, many people are online natives that will never step foot in a physical bank. Banks can offer checking, savings, and lending online thanks to the internet.

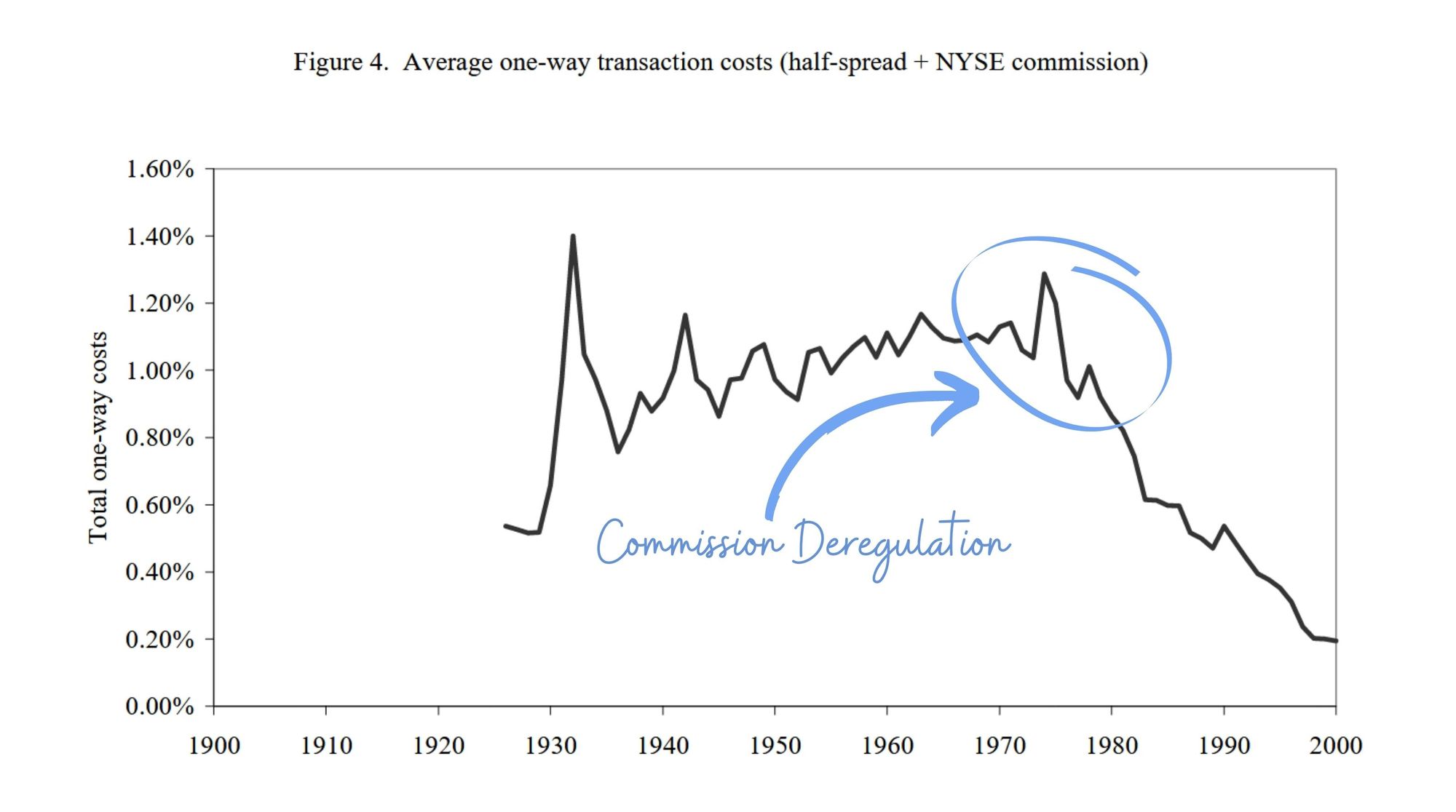

On the investing side, finance jumps at the opportunity to transact faster. The stock market has evolved from human brokers receiving and routing orders by phone on a sheet of paper to automated electronic trades using an order book to match buyers and sellers. Price discovery used to depend on the broker's skill, but now brokerages offer real-time prices for free.

Finance has done a lot and reinvented itself many times throughout history. But though it seems like finance continues to progress with technology, the industry doesn't look all that different. Over the last decade, technology has advanced, but financial technology in the United States has struggled to keep up.

In the U.S., much of the innovation we've seen in banking over the last decade has been good, but they haven't been disruptive. Most online banks, like Chime, aren't real banks. On the backend, they leverage traditional white-label banks. They're very innovative because they can focus on technology without worrying too much about regulation. But many conventional banks have no reason to blink as long as online banks built their systems atop the legacy mountain. Big banks continue to thrive by doing the bare minimum — having a presence online and on mobile. They continue to require minimum balances and charge overdraft fees. In 2019, banks brought in $34.6 billion in overdraft revenue alone [1]. That number increased every year since 2011.

On the investing side, brokerages felt Robinhood's impact in 2019 when they all decided to stop charging commission fees [2]. At the time of the seemingly unanimous decision, commissions accounted for 15% of TD Ameritrade's revenues and 11% of E-Trade's. It was disruptive because these brokerages were left with two options, both unattractive: drop 10% of your revenue immediately or slowly die from price competition over time. No business wants to be in that position, but they had to react. Charles Schwab, who triggered the final push to zero, acquired TD Ameritrade in 2020, and Morgan Stanley acquired E-Trade.

Robinhood played a critical role in getting the number down to zero, but commissions had been steadily declining since 1975 due to deregulation. The race to zero commissions started decades before Robinhood was founded. Regulatory hurdles that would have prevented their survival had already been cleared. Robinhood disrupted the space even though they accelerated the inevitable.

Zero commission brokerages, neobanks, and many consumer fintech companies have done exceptionally well on their approach to simplicity. Anyone can become a user in only a few minutes, and everyone can become an expert. Compared to their legacy counterparts, these fintech companies have removed learning curves from their apps. These changes make finance more accessible, but the features we see today are not all that different from what existed in the past.

We've been here before. eBanking was a thing in the 90s. These were online banks that were very similar to today's neobanks in every way but looks. They had no branches, offered higher interest rates, and low or no fees. They no longer exist thanks to the internet bubble of '99 and the subsequent financial crisis of '08. Many ebanks were launched as a digital version of traditional banks back then. The internet wasn't a guaranteed success yet, especially not after the crash. Big banks didn't sweat back then, and they aren't sweating now. Unlike what happened with zero commissions, zero overdraft fees din't threaten big banks. If neobanks disrupted anything, it wasn't their predecessors.

Fintech has done a lot so far, but founders limited their scope of innovation to what can be built on the legacy infrastructure. They continue to rely on those they should be disrupting. I recently realized it. Fintech seemed like the most innovative way for finance to interop with technology till I tried DeFi. It got me thinking about what fintech companies would look like today had they not relied on legacy infrastructure. I didn't have to think too hard because those companies exist today (We'll get into this in Part 3).

FinTech 1.0 is now mature. Vertical companies now have to compete with those starting to go horizontal with their products. For example, Chime now has to compete with Robinhood's Cash Management. This maturity is most visible with Stripe. They've gone from offering just payments to, well, everything. In one way or another, Stripe now competes with several fintech players.

FinTech 2.0 or finance-as-a-service is ushering in a world where every app has finance embedded. A typical but good example is the wallet in the Uber app. Funds in your Uber Wallet can be used throughout the Uber ecosystem. They can be spent on rideshare, Uber eats, and Postmates.

Every company becoming a fintech company shows how fintech is maturing. All this has happened without significant disruption to incumbents. But things are starting to change.

In 2018, Robinhood launched its own clearing system. According to co-CEO and co-founder Vlad Tenev [5]:

It’s the only system that has been built from scratch on modern technology in the past decade. It’s a huge investment in the future of Robinhood.

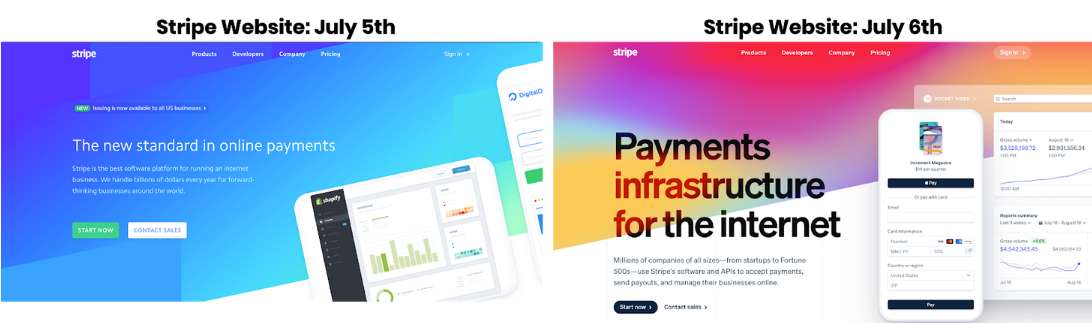

In 2020, Stripe announced that they now connect directly to Visa, Mastercard, AMEX, Discover, JCB, and China Union Pay across global markets. According to their press release [6]:

By exchanging information directly with the card networks, rather than relying on intermediaries, Stripe can reduce latency and remove potential points of failure for its customers.

That same year, they also made a significant change to their homepage going from "The new standard in online payments" to "Payments infrastructure for the internet."

And finally, also in 2020, neobank Varo became a licensed bank. According to Business Insider [7], to exit its partnership with The Bancorp Bank, Varo had to repurchase its customer's data to migrate them. That aside, Varo can now directly offer bank accounts, credit cards, loans, and home financing.

Fintech companies had to rely on legacy infrastructure till they were mature enough to build their own. The next decade should show us what can be created with new primitives. It's exciting, but at the same time, we already have new upstarts in the DeFi world. Those upstarts have already solved many of the problems fintech will tackle in the next decade.

In Part 2, I'll discuss some of the problems I think fintech will start to tackle. Some are technical, but most are regulatory. I'll provide an example comparing two blow-ups: one on the legacy system, and the other on smart contracts.

In part 3, I'll dive into some of the companies (protocols) that have already solved the technical problems but are still facing regulatory uncertainty.

Subscribe to get the next post in your email | Read More Of My Writing | Read What I'm Reading

The following tweet should prepare you for some of the topics I'll cover.

Example of an August 25, 1873 "telegraph transfer." Note the cost is 3% (and it took 2 to 4 days).

— Jim Bianco (@biancoresearch) June 21, 2021

Today bank wire transfers still cost about 3% and take a few days. Credit card fees are also 3%.

No change in 150 years. pic.twitter.com/YydhGDMOjK

Sources

[1] 2019 Overdraft Fees — https://www.wsj.com/articles/overdraft-fees-fell-in-the-covid-19-economy-11622367000?mod=article_inline

[2] 2019 Wave of 0 commissions — https://www.wsj.com/articles/the-race-to-zero-commissions-11570267802

[3] A CENTURY OF STOCK MARKET LIQUIDITY AND TRADING COSTS (PAPER) — https://www0.gsb.columbia.edu/mygsb/faculty/research/pubfiles/4048/A century of Market Liquidity and Trading Costs.pdf

[4] NetBank — https://web.archive.org/web/20070818121749/http://www.netbank.com/index.htm

[5] Robinhood Clearing — https://www.cnbc.com/2018/10/10/robinhood-launches-its-own-trade-clearing-system-as-customer-growth-surges.html

[6] Stripe Press Release — https://stripe.com/newsroom/news/direct-platform

[7] Varo — https://www.businessinsider.com/varo-attains-us-national-bank-charter-2020-8