Betting on Irrationality - the toilet paper IPO

Was investor reaction to the coronavirus unprecedented? Or was it more of the same?

In one of the newsletters I sent out in March, I tried making a case for why the S&P 500 index might end the year positively. That was amid the market panic with soaring volatility that sent shares tumbling. Now, months later, the index is well into the green. The coronavirus is still present, but it has largely been forgotten by investors. The 0% interest rate environment and the stimulus package have helped restore confidence in the market. But the FED is only effective due to human behavior. They could inject as much stimulus as they want, but the market won't recover unless its participants are optimistic. People, their emotions, and expectations move the market. Institutional funds may be trading and holding a bulk of securities, but the underlying capital belongs to human beings with irrational emotions. In today's note, I'll attempt to breakdown the reasoning behind that guess. Before getting into it, I'd like to clarify what I won't be writing about.

Behavior, not economics - though they played some role, I won't be writing about technical analysis, company fundamentals, macro- or micro-economics,. I'm not disregarding them, they're individually and collectively important. Rather, I'm avoiding them because I wasn't focused on them back in March.

Process, not outcome - when it comes to making decisions, the process is more important than the outcome. You can bet on who will win the Superbowl, but you can't influence the outcome from your couch. The same thing goes when risking money in the market, nobody knows because the possibilities are endless. Instead of trying to imagine or model a million outcomes, I find it easier to focus on what I can control.

The stock market, not the economy - I bet on the stock market recovering. I won't even pretend to understand everything going on with the economy.

Pre-Read - I usually do a terrible job of documenting my decision-making process, and this time was no exception. My personal notes and research are fragmented but luckily I sent out that relevant newsletter on March 7. I'll be referencing it to help make a little more sense of my process. I recommend reading that before continuing. It should take less than 5 minutes.

In most of our decisions, we are not betting against another person. Rather, we are betting against all the future versions of ourselves that we are not choosing. — Annie Duke, Thinking in Bets

Availability Cascade

As global markets tumbled, I wanted some clarity on where we'd be by the end of the year. On February 29, I wrote to subscribers, urging investors to be empathetic instead of writing off the virus as yet another common flu. Losing money doesn't compare to losing loved ones. I also cautioned against senseless buying because things looked cheap. I was optimistic. I didn't think the epidemic would become a pandemic, but that particular drop did not look like a buying opportunity. In retrospect, buying then would have hurt more than doing nothing.

On March 7, I wrote about volatility and uncertainty. I explained how any news other than a vaccine is bad news, and how the virus could continue to drive prices lower. That was due to the availability cascade — higher case and death counts lead to more media coverage which leads to more panic selling which, in turn, grabs more media attention and leads to even more selling and so on. Just think, how many times did you hear the word unprecedented prior to February 2020?

Human Behavior is Predictable

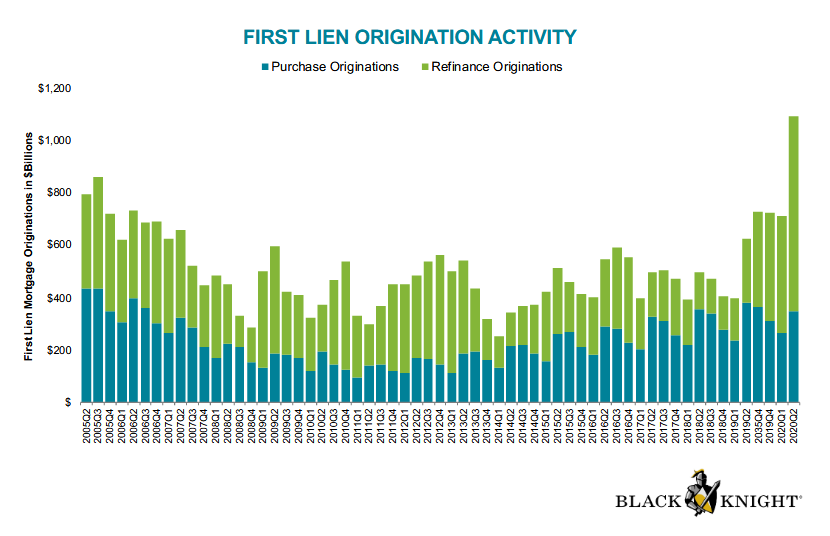

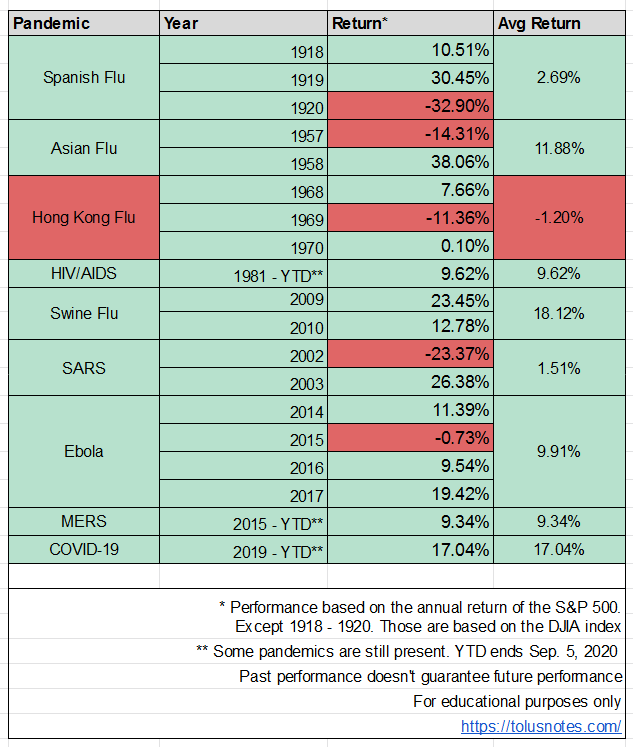

Reading and researching how the market behaved during past pandemics helped me form the base case for my guess. As unprecedented as the economic standstill may have been, investor behavior was very consistent. The FED expected investors to borrow and spend more when interest rates are lower. They also expected investors to take on equity risk premium when fixed income returns are next to nothing. Investors delivered on both fronts. According to BlackKnight, mortgage refinance lending is up 200% YOY. We'd be in a different position today if people didn't react to cheap capital.

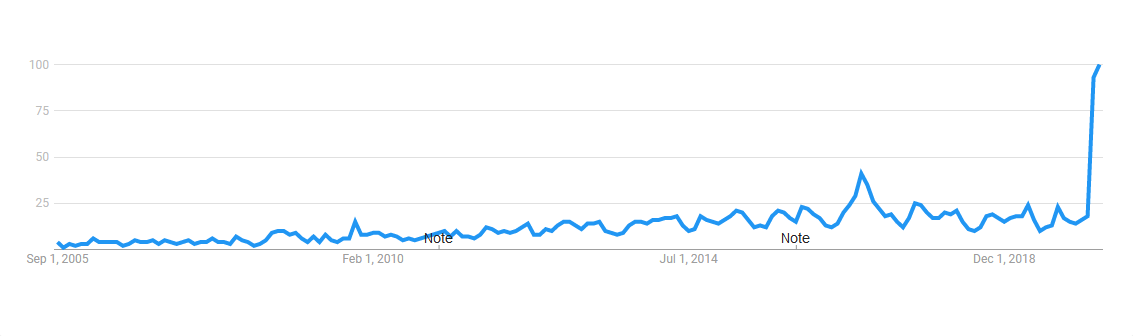

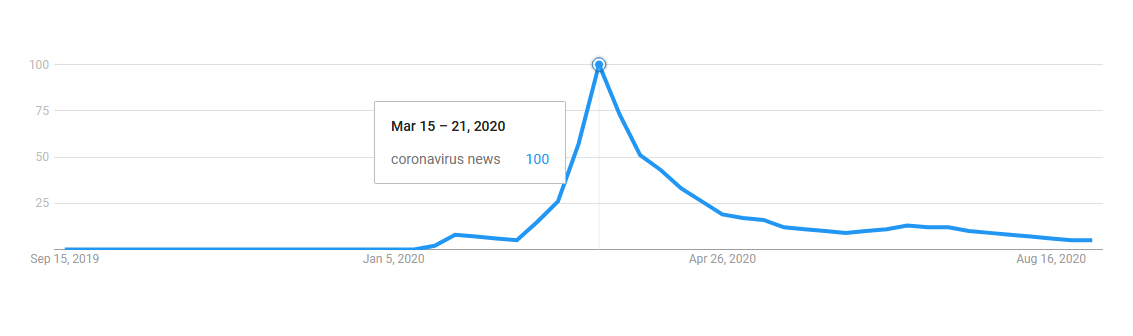

Similarly, I expected the news to headline topics other than the coronavirus as soon as something more interesting happened. It's a feature of the media. They lose ad revenue and subscribers if they don't cover hot topics. At the time, I still believed that the virus would be contained, so it seemed likely that the media would no longer find it interesting. Things obviously didn't play out that way. The virus was upgraded to a pandemic the following week, and the market fell more as a result. Circuit breakers were a constant reminder that things weren't getting any better. The availability cascade got even worse as the media had something new (pandemic vs epidemic) to report. But like clockwork, things reversed. The interest in news articles about the virus peaked on March 21, the S&P 500 bottomed out on March 23. It's most likely a coincidence, but my point is that the availability cascade can also work in reverse. The media stops reporting on the virus which leads to people feeling better about the situation which leads to general optimism that affects investment decisions which, in turn, leads to more good news about market returns, and less about the virus.

Risk Assessment: the Toilet Paper IPO

The worst thing that could have happened was complete ruin — losing everything. The likelihood of it happening was really low, but not 0%. People sold when they realized that the threat of losing money was real. When some realized that society might crumble, they sold some more equities and loaded up on toilet paper and canned beans. But if society crumbled, the dollar will no longer hold any value. Not in the U.S, and not overseas.

Older people freaking out was OK. They may have been close to or at retirement, and the virus was hitting them harder compared to other age groups. But the overreaction from young investors was irrational. Something younger investors need to keep in mind is that unrealized market returns are ephemeral and thus, irrelevant. Unless the money is being withdrawn, the returns are just eye candy. Bull markets benefit those withdrawing money from their accounts. Young investors that are accumulating are actually worse off. Think about it, accumulators are buying high while retirees are spending high. Wouldn't you rather buy low? As financial theorist and neurologist, William Bernstein puts it: young investors should pray for a long bear market.

Human beings suck at judging risks. It's why some people never invest their money in the stock market, but swear by the lottery. It's why some investors regularly buy puts to hedge against volatility in their portfolio. Both groups severely miscalculate the chances of losing money because most lottery tickets aren't winners, and most hedges are only there to support human emotion. If they understood the risk, the lottery buyer will do literally anything else with his money, and the investor will balance the risk exposure in her portfolio.

Investors are cursed with short term memory. Most looking to outsmart the market without understanding its history lose money. Economics and financials aren't enough, people and their emotions are behind everything that happens. At the end of the day, I'd rather bet on people acting irrational instead of trying to predict the market.

✉️ Thanks for reading. Let me know what you think of it at newsletter@tolusnotes.com

❤️ If you enjoyed it, please forward it to support the newsletter.

👊 If this was forwarded to you, you can subscribe here for future notes

📚 Currently reading Homo Deus: A Brief History of Tomorrow

📚 Also rereading My Favorite Stock Market Book

Tolusnotes participates in Amazon Services LLC Associates Program. We earn a small revenue from qualifying purchases.